Executive Summary

Every Singapore employer faces four non-negotiable payroll obligations each month and year: CPF contributions, Skills Development Levy (SDL), MOM-compliant itemised payslips, and annual IRAS income tax reporting via IR8A or the Auto-Inclusion Scheme (AIS). Missing any one of these can result in backdated payments, financial penalties, or prosecution under the Income Tax Act.

This guide covers every obligation in plain terms. You’ll find the current 2026 CPF contribution rates and wage ceilings, SDL calculation rules, MOM payslip requirements, IR8A deadlines and penalties, and a ready-to-use compliance checklist. Where payroll software automates these obligations, we reference what to look for in a solution built for Singapore SMEs, including Rockbell’s Million Payroll and supporting HR suite products.

The Employment Act: Your Payroll Foundation

The Employment Act is Singapore’s primary payroll legislation. It covers all employees working under a contract of service, whether permanent or contract, full-time or part-time, local or foreign. The main exceptions are managers and executives earning above S$4,500 per month, domestic workers, and seafarers.

Three obligations sit at the core of the Act for every SME employer.

Salary payment timing. Employers must pay salaries at least once a month and within seven days after the end of the salary period. Overtime pay has a separate deadline: within 14 days after the salary period ends.

Written employment contracts. Employers must provide written contracts within two months of an employee’s start date. The contract should clearly state allowances (housing, transport, meals), since these may attract CPF contributions and income tax.

Itemised payslips. Since 1 April 2016, every employer covered by the Act must issue an itemised payslip to every employee. The MOM requires 12 specific data points — discussed fully in the SDL and MOM compliance section below.

Non-compliance with the Employment Act exposes employers to penalties and legal action from employees or the Ministry of Manpower. Enforcement is active: IRAS prosecuted 1,207 repeat payroll offenders in 2025, resulting in penalties exceeding S$1 million (source: Harvest Accounting).

CPF Contributions: Rates, Ceilings & Deadlines

CPF is a compulsory social security savings scheme. Employers must contribute on behalf of all Singapore Citizens and Permanent Residents employed under a contract of service. Foreign employees on work passes (EP, S Pass, Work Permit) are exempt from CPF, but employers remain liable for SDL and, where applicable, the Foreign Worker Levy.

2026 CPF Contribution Rates

Rates vary by employee age. The table below reflects rates effective 1 January 2026 (source: CPF Board via Harvest Accounting):

| Employee Age | Employer Rate | Employee Rate | Total

|

|---|---|---|---|

| 55 and below | 17% | 20% | 37% |

| Above 55 to 60 | 16% | 18% | 34% |

| Above 60 to 65 | 12.5% | 12.5% | 25% |

| Above 65 to 70 | 9% | 7.5% | 16.5% |

| Above 70 | 7.5% | 5% | 12.5% |

From 1 January 2026, the employer’s share for workers aged above 55 to 65 rose by 0.5 percentage points versus 2025 rates.

2026 Wage Ceilings

Two ceilings govern how much of an employee’s salary is subject to CPF:

- Ordinary Wage (OW) Ceiling: S$8,000 per month (raised from S$7,400 in 2025)

- Annual CPF Salary Ceiling: S$102,000 per year

- Additional Wage (AW) Ceiling: S$102,000 minus total ordinary wages on which CPF was already contributed during the year

Ordinary Wages are wages paid wholly for work done in the salary month, including basic salary and fixed monthly allowances. Additional Wages are paid at intervals greater than one month, such as annual bonuses, AWS, and quarterly commissions. Misclassifying OW as AW (or vice versa) is the single most common cause of CPF underpayment in Singapore.

CPF Payment Deadline and Penalties

CPF contributions are due by the 14th of the following month. If the 14th falls on a weekend or public holiday, the deadline rolls to the next working day. Late payment attracts a 1.5% penalty per month (18% annualised), with a minimum charge of S$5. Persistent non-payment can result in prosecution.

CPF is not payable on employees earning S$750 per month or below.

SDL Contributions and MOM Compliance for Singapore SMEs

Skills Development Levy (SDL)

The SDL is a mandatory monthly levy all Singapore employers must pay for every employee rendering services in Singapore, including foreign workers on EP, S Pass, and Work Permit. It is collected by the CPF Board on behalf of SkillsFuture Singapore Agency and funds workforce training grants under the National Continuing Education Training system.

SDL rate: 0.25% of each employee’s total monthly wages

- Minimum: S$2 per employee per month (for wages below S$800)

- Maximum: S$11.25 per employee per month (for wages above S$4,500)

As a practical example: if you have ten employees each earning S$4,000 per month, your total monthly SDL is S$100, or S$1,200 per year (source: Harvest Accounting).

SDL covers all employment types: full-time, part-time, casual, temporary, and contract. The only exemptions are domestic servants, chauffeurs, and gardeners hired for personal (non-business) use, and employees who performed no services in Singapore for an entire calendar month.

Payment deadline: Within 14 days from the end of each month. Late payment carries a 10% per annum penalty on the outstanding amount and may affect your organisation’s eligibility for SkillsFuture training grants.

How to pay SDL: For most employers, SDL is submitted alongside CPF contributions via CPF EZPay (using SingPass or CorpPass). The system auto-computes SDL for Singapore Citizens and PRs; amounts for foreign employees must be entered manually. Employers with only foreign staff should use the GoBusiness SDL e-payment portal.

MOM Payroll Obligations: Itemised Payslip Requirements

Under the Employment Act, every payslip must include these 12 items (source: Harvest Accounting, MOM):

- Employer’s full name and address

- Employee’s full name

- Payment date

- Salary period (start and end date)

- Basic salary or hourly rate and hours worked

- All fixed allowances (transport, housing)

- Ad-hoc allowances (overtime pay, bonuses)

- All deductions, including CPF employee share and unpaid absences

- Overtime hours worked

- Overtime pay amount

- Overtime payment period if different from the salary period

- Net salary paid

Payslips must be issued with salary payment or within three working days. Both digital and paper formats are acceptable. PDF via email satisfies the requirement.

Record retention: Payslips and employment records must be kept for at least two years for current employees, and at least two years after departure for former employees. CPF records must be retained for at least five years.

Issuing an incomplete payslip is an Employment Act violation, even if the salary itself was paid correctly and on time.

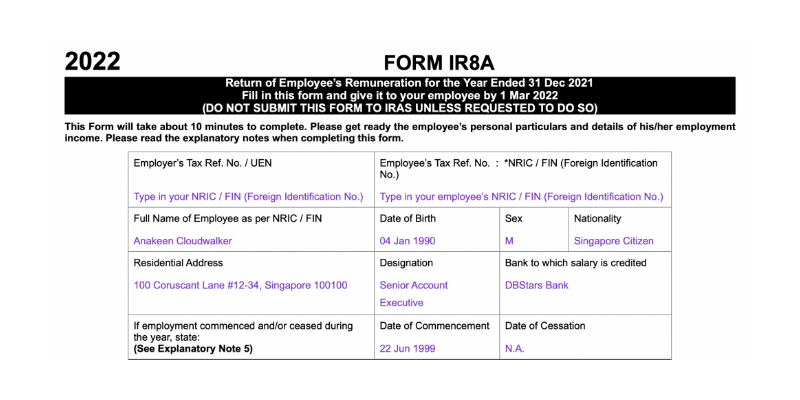

IRAS Income Tax Reporting: IR8A and the Auto-Inclusion Scheme

Every Singapore employer must report each employee’s total annual earnings to IRAS via Form IR8A by 1 March each year, covering income earned in the previous calendar year.

Who Must File IR8A

IR8A is required for all employees who received income during the reporting year, regardless of employment status or residency:

- Full-time and part-time resident employees

- Non-resident employees

- Company directors, including non-resident directors

- Board or committee members receiving fees

- Pensioners

- Former employees who received income in the reporting year (for example, a bonus paid after resignation)

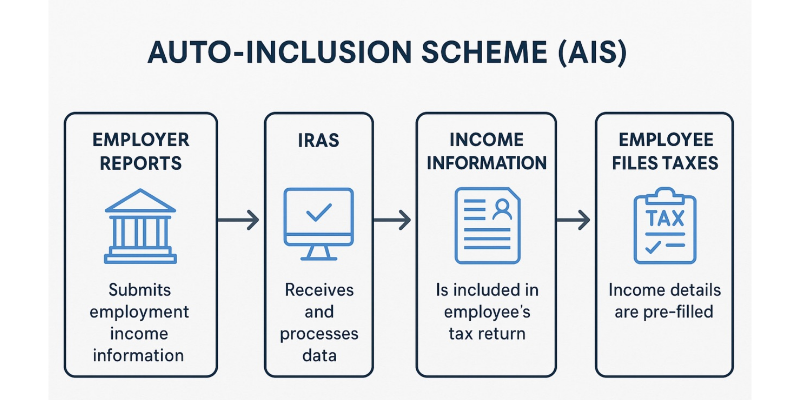

Auto-Inclusion Scheme (AIS)

Employers with five or more employees are mandatorily on AIS from YA2026 onward. Under AIS, employment income data is submitted electronically through the myTax Portal, which pre-fills employees’ personal tax returns. Employees covered by AIS do not need to manually declare their employment income.

Employers below the five-employee threshold may join AIS voluntarily. Those who do not must hand each employee a physical or digital IR8A by 1 March.

Penalties for Non-Compliance

Failing to file IR8A on time is a criminal offence under the Income Tax Act. Penalties include:

- Fines of up to S$5,000 for first offences

- Up to S$10,000 and up to 12 months’ imprisonment for repeat offences

- IRAS may issue estimated assessments, creating complications for employees

There is no grace period and no informal warning system.

Related IRAS Forms

Three additional forms may apply depending on your workforce:

- Appendix 8A: Required for employees receiving non-cash benefits such as housing, company cars, gifts, or personal expense reimbursements

- Appendix 8B: Required for employees with gains from Employee Stock Options or share award plans

- IR8S: Required where CPF contributions exceeded the statutory cap or an employee was posted overseas while CPF was still being contributed

For non-Singaporean employees leaving employment or Singapore, employers must also file Form IR21 (tax clearance) at least one month before the employee’s cessation date. All monies owed must be withheld until IRAS issues a clearance directive.

Payroll Compliance Calendar

| Frequency | Deadline | Obligation

|

|---|---|---|

| Monthly | Within 7 days of salary period end | Pay employee salaries |

| Monthly | Within 3 working days of payment | Issue itemised payslip |

| Monthly | 14th of following month | Submit CPF contributions |

| Monthly | 14th of following month | Pay SDL |

| Annual | 1 March | Submit IR8A / AIS data to IRAS |

| On employee departure | At least 1 month before last day | File IR21 for non-Singaporean employees |

If the 14th falls on a weekend or public holiday, CPF and SDL deadlines roll to the next working day. There are no extensions for the 1 March IR8A deadline.

Six Common Payroll Mistakes Singapore SMEs Make

Knowing the rules is one thing. Applying them consistently under deadline pressure is another. These are the six most frequent errors, based on MOM enforcement patterns and IRAS audit data (source: Harvest Accounting, Raffles Corporate Services):

- Using outdated CPF contribution rates. Rates change annually and shift at age thresholds of 55, 60, 65, and 70. A 56-year-old employee who turns 60 mid-year needs a rate adjustment in the correct month.

- Misclassifying OW and AW. Year-end bonuses exceeding the Additional Wage ceiling are the most common source of CPF underpayment. Run a year-to-date AW reconciliation each November to catch shortfalls before December payroll.

- Missing the 1 March IR8A deadline. IRAS does not grant extensions as a matter of course. Late submission is a criminal offence, not an administrative oversight.

- Issuing incomplete payslips. Omitting any of the 12 MOM-required items violates the Employment Act, regardless of whether the amounts themselves are correct.

- Misclassifying employees as contractors. IRAS and MOM apply multi-factor tests covering control, integration, and exclusivity to determine employment status. Getting this wrong means backdated CPF, SDL, and potential prosecution.

- Forgetting SDL for foreign employees. SDL applies to all employees, not just Citizens and PRs. Many SMEs accurately compute CPF but overlook SDL for their foreign workforce.

Payroll Software vs. Manual Payroll: What Works for Singapore SMEs

Manual payroll using spreadsheets can work for a business with two or three employees and a straightforward pay structure. But it carries real risks at scale: spreadsheets have no audit trail, CPF rate tables must be updated manually, and a single formula error can compound across months before anyone notices.

Payroll software built for Singapore automatically calculates CPF at current rates and wage ceilings, computes SDL for both local and foreign employees, generates MOM-compliant payslips, and prepares IR8A data for AIS submission.

Rockbell’s Million Payroll is built specifically for the Singapore compliance environment. The Million HR Suite covers five distinct functions: payroll processing, leave management, claims management, appraisals, and time attendance. Biometric hardware integration is also available for SMEs managing shift-based or site-based teams.

For SMEs comparing their options more broadly, Rockbell’s guide Payroll Software in Singapore vs. Manual Payroll: What Works Best for SMEs? works through the cost and compliance trade-offs in detail. If you’re weighing software against outsourcing entirely, Payroll Software vs. Outsourced Payroll Services: Which Supports SME Growth Better in 2026? covers that comparison directly.

For a broader market view, Rockbell also publishes The 10 Best Payroll Software in Singapore (2025) if you want to evaluate the full range of options available to Singapore SMEs.

The cost case for software is straightforward. An in-house payroll hire costs S$30,000 to S$45,000 or more per year (salary plus employer CPF). A payroll software solution for ten employees typically runs well below that, and eliminates the compliance knowledge dependency on one individual (source: Harvest Accounting).

Compliance Checklist for Singapore SMEs

Use this checklist each month and at year-end to confirm you’ve met every statutory obligation.

Monthly Obligations

- Salaries paid within 7 days of salary period end

- Itemised payslip issued within 3 working days of payment, including all 12 MOM-required items

- CPF contributions calculated at correct rates for each employee’s age band and OW ceiling (S$8,000/month from January 2026)

- SDL computed at 0.25% of total wages per employee (min S$2, max S$11.25), including foreign employees

- CPF and SDL submitted and paid by the 14th of the following month

- Foreign Worker Levy paid for all S Pass and Work Permit holders (where applicable)

Annual Obligations

- Year-to-date OW and AW reconciliation completed by November to catch CPF ceiling issues before December

- IR8A or AIS submission completed by 1 March for all employees (mandatory AIS if 5+ employees)

- Appendix 8A filed for any employees who received non-cash benefits

- Appendix 8B filed for any employees with stock option or share award gains

- IR21 filed at least one month before any non-Singaporean employee’s departure

Record-Keeping

- Payslips and employment records retained for at least 2 years (current employees) or 2 years post-departure (former employees)

- CPF records retained for at least 5 years

- Written employment contracts on file for all employees

Frequently Asked Questions (FAQs)

What are the CPF, SDL, MOM, and IRAS payroll obligations for Singapore SMEs?

Singapore SMEs face four core statutory obligations. CPF contributions must be paid by the 14th of each month for all Singapore Citizen and PR employees, at rates ranging from 12.5% to 37% of salary depending on age. SDL must be paid for every employee, including foreign workers, at 0.25% of monthly wages (minimum S$2, maximum S$11.25 per employee). MOM requires employers to issue itemised payslips covering 12 mandatory data points within three working days of each salary payment. IRAS requires annual IR8A or AIS submission by 1 March covering all employees’ income from the previous calendar year. Employers with five or more employees must submit via AIS electronically.

Who is required to pay CPF contributions in Singapore?

Employers must contribute to CPF for all Singapore Citizens and Permanent Residents employed under a contract of service. Foreign employees on Employment Passes, S Passes, or Work Permits are not covered by CPF. However, employers remain liable for SDL on all employees regardless of nationality or pass type.

What is the SDL rate in Singapore and who must pay it?

SDL is set at 0.25% of each employee’s total monthly wages. The minimum payment is S$2 per employee per month (for those earning below S$800) and the maximum is S$11.25 per employee per month (for those earning above S$4,500). Every employer in Singapore must pay SDL for all employees, including foreign workers, part-timers, and temporary staff. Payment is due within 14 days of each month-end, and late payment attracts a 10% per annum penalty.

When is the IR8A deadline and what happens if I miss it?

IR8A or AIS data must be submitted to IRAS by 1 March each year, covering income paid in the previous calendar year. There is no grace period. Missing the deadline is a criminal offence under the Income Tax Act, carrying fines of up to S$5,000 for a first offence and up to S$10,000 plus possible imprisonment for repeat non-compliance. Employers with five or more employees must submit electronically through the Auto-Inclusion Scheme via the myTax Portal.

Can payroll software handle CPF and SDL submissions automatically for Singapore SMEs?

Yes. Payroll software designed for Singapore, such as Rockbell’s Million Payroll, calculates CPF contributions at the correct rates and wage ceilings for each employee’s age band, computes SDL for both local and foreign employees, generates MOM-compliant itemised payslips, and prepares IR8A data for AIS submission. This reduces the risk of manual errors, which are the leading cause of CPF underpayment and MOM non-compliance for SMEs. For a full comparison of software versus manual payroll, see Rockbell’s guide on Payroll Software in Singapore vs. Manual Payroll.